This article was published on Investopedia

The financial advisory industry uses different business models to compensate industry professionals. The difference in compensation determines a lot about how they interact with clients. Three of the more common industry models are broker-dealers, Registered Investment Advisors (RIAs) and hybrid advisors.

Read more: The Difference Between Brokers and RIAs

This article was published on Investopedia

Helping more people access retirement planning is a noble cause, especially when you consider 30% of eligible employees do not participate in their employer’s 401(k) plan. Given the many savings and tax advantages of these plans, one would expect 100% participation.

Read more: 5 Ways to Increase Employee 401(k) Plan Participation

This article was published on Investopedia

Margaret S. faced the ultimate thief. She lost her husband to a sudden cardiac arrest. Only 59 and in seemingly good health, at least he had the foresight to keep a million-dollar life insurance policy on himself, naming her as beneficiary. Referred to us by a friend, Margaret arrived at our first appointment shaken and afraid. Not only was she grieving the loss of her life partner, she now faced a torrent of consequences from this sudden windfall of money.

Read more: Irrevocable Life Insurance Trust: Protect Your Estate

Margaret S. faced the ultimate thief.

She lost her husband to a sudden cardiac arrest.

Only 59, in seemingly good health, at least he had the foresight to place a million-dollar life insurance policy on himself, naming her as beneficiary. Referred to us by a friend, Margaret arrived at our first appointment shaken and afraid.

Not only was she grieving the loss of her life partner, she now faced a torrent of consequences from this sudden windfall of money.

The IRS demanded its sizable share of the proceeds to cover tax liability.

And creditors demanded the rest to pay off debts she didn’t even know her husband had.

How would she provide for herself and her three children?

I wish I could tell you this situation is uncommon. In fact, it is all too common.

More than half of all Americans do not have a will or an estate plan.

An unbelievable 92 percent of adults under age 35 do not have a will or estate plan.

Sadly, it was too late to help Margaret.

But it is not too late to help you.

I want to introduce you to a powerful device called the Irrevocable Life Insurance Trust, ILIT for short.

Think of an ILIT as a holding device that owns your life insurance policy for you, thus removing it from your estate. Everything you own in your name at death the government includes in your estate for tax purposes.

Like its name, once you set up an ILIT, and place your life insurance policy(ies) in it, you cannot take them back, at least in your own name.

ILITs offer the flexibility you need to name beneficiaries, stipulate the terms by which they receive benefits, and you can choose the trustee you wish to manage this device. It is critical to design the ILIT correctly and to follow all guidelines.

We strongly believe in the efficacy of ILITs to wipe away the messy problems that can stain the estate planning effort. Consider these beneficial solutions:

Laws vary from state to state, so it is important to sit down with your attorney and us to determine what best fits your circumstances. We can assist you in:

A brief word about the role of the trustee. He or she manages your ILIT and will follow your directions. Whatever money you transfer to the ILIT annually, your trustee uses it to pay insurance premiums. Your trustee handles a variety of administrative actions like the annual notification to beneficiaries (the “Crummey Letter”) and files the ILIT’s tax return.

Once we set up your ILIT, we will also help you make an informed choice on the right life insurance policy to place in the device. You may select an individual policy of a second-to-die (survivorship) policy. Remember, you do not pay the premiums directly; the trustee handles that for you.

There are many smaller decisions to make in drafting your ILIT:

Whether you can use an existing policy; what to do regards gifting and the gift tax exclusion; and if your policy avoids probate, areas we explain in a private meeting.

What do you do if you don’t wish to keep the ILIT in force any longer?

Rest assured, you are not required to continue making premium payments. Your policy may lapse as soon as you miss your annual premium payment, depending on its type. If it is a cash value arrangement, the funds may be used to pay premiums until you exhaust all the accumulated cash.

A final word in this very brief tutorial.

Because you cannot transfer a policy owned by an ILIT into your own name, if you think you ever need to or need to tap the cash value, think carefully. The ILIT may not be a smart strategy for you.

Look forward to discussing an ILIT and other strategies with you in the future.

[Note: Margaret S. is a fictitious character created for purposes of illustration]

To Your Financial Freedom,

The Roush Group

O: 559.579.1490 F: (559) 490-2015 C: (559) 285-3318

As employers prepare for open enrollment season, those wanting to boost participation in their 401(k) plans should act now to deploy strategies that work.

Helping more people access retirement planning is a noble cause, especially when you consider 30 percent of eligible employees do not participate in their employer’s 401(k) plan. Sad to say.

Given the many savings and tax advantages of these plans, one would expect 100 percent participation.

What’s the problem?

Better yet, what’s the solution?

Well, the answer to the first question is bit complex. And it involves the expanding field of behavioral finance, too hefty for this quick post.

My goal for this post? Simplify the complex for you and your employees.

That’s why we will not discuss reasons why only ten percent of employers with fewer than 100 employees offer a 401(k) plan, at all. And I will not tackle why eligible employees who do participate don’t save enough. Or why employees need to resist borrowing from their 401(k) plans.

Two reasons drive one-third of workers to shut themselves out of at least some retirement security: 1) The process seems complicated, and 2) humans tend toward short-term thinking.

In a useful survey from AARP, more than half of adults said they had made an investment with an adverse outcome because they “didn’t understand” the investment, which negatively affected their appetite for saving into a retirement plan. It turns out the adverse outcome was based on unexpected taxes or a penalty on early withdrawal─easily overcome had these consequences been communicated clearly and early on.

But here’s the rub. Of those surveyed, 54 percent admitted they “don’t read financial literature because it is too hard to understand.”

In another study by the Social Security Office of Policy, we learn that short-term goals have a negative impact on participation rates. The study establishes that employees’ planning horizon matters. For example, those who “plan for periods of less than five years are much less likely to provide for their retirement than those who have a longer perspective.”

Do you see what a challenge these realities present for everyone in the retirement planning business? Then, add inertia to the challenge. Given the option to do nothing, most people will do nothing, even if the choice brings good to them.

It is extremely difficult to change someone’s opinion, let alone change their behavior. However, we must try. We have an obligation as good stewards of retirement planning to give employees every conceivable opportunity to retire with dignity.

As an employer offering a 401(k) plan, you took a major step forward in the retirement challenge. Now, let us work with you to help you engage more of your workforce in your plan so they can realize the long-term benefits of the plan you’ve so generously provided.

Here are some simplified strategies you can put into play to help your company experience a successful enrollment season. And keep in mind, we want to minimize fears and misconceptions around 401(k) plans.

I could share 50 more ways to increase your plan participation; this whirlwind post only touches the surface. However, if you do these five things I’ve suggested, you’ll feel a tailwind at your back and head in the right direction.

In the meantime, talk to us about any special challenges you face. And remember, you can always outsource full 401(k) plan design, implementation and administration (including employee education and communication) to a specialty firm, like ours.

Ask us about our innovative DCPro program, which brings together in an exceptional alliance the best of the best plan fiduciaries in the business.

To Your Financial Freedom,

Roush Investment Group

O: 559.579.1490 F: (559) 490-2015 C: (559) 285-3318

When I spend time at our lake house, I think a lot.

One afternoon, I sat quietly watching the clouds reflect off ripples moving across the lake. I felt nostalgic. I wanted to pen a note to my daughter, Jessica.

I wanted to tell her how to live life without regret.

I’ve had my own. But I wanted to spare her the regrets so many of us experience when life falls short of its full potential.

Jessica is strong, smart and well into her career. I know she will do well in life. What could become her regrets, I wondered. And could I help her?

Then, I began to think about you─our clients, your families and what regrets you might be shouldering at this moment.

In her book The Top Five Regrets of the Dying, palliative care nurse Bronnie Ware shares the thoughts of her patients as they prepared for their quiet endings.

What matters most at this point?

And why would a financial advisor like me dare to comment on such a sacred subject?

Here is Ms. Ware’s list of the top five regrets (think wishes) of the dying:

Do you see yourself in these thoughts? Are they meaningful to you?

Do you notice not one is about money?

Although I am in the business to manage money, grow and preserve wealth, I find myself surrounded by the emotional side of money every day.

The freedom it brings. The responsibility. The stress. The fear of loss.

So I counsel my clients, usually by asking many difficult questions. I need to know you not only on a financial level but on an emotional level, too.

And now I want to learn how my skills at financial advisory can help you live life without regrets.

Most credit Mark Twain with saying: I believe we feel the most regret about missed chances we did not take.

That’s because our “psychological immune system” allows us to recover from unpleasant experiences more quickly than we think due to our ability to rationalize and reframe how we view things. However, it is harder for this system to kick in when we have never tried something in the first place.

Let’s talk about the things you can do now to diminish regrets in your life on an emotional level; then we’ll talk about tangible things you can do on a financial level to buffer you from regrets later.

Here’s a personal roundup of seven areas I work on to reduce the potential for regret:

Write down what you believe you can do now to leave no regrets.

It is a very personal process, just like financial life planning. Give it a try. It can be liberating.

Now, let’s turn to the practical side of regret-banishing. There are certain financial actions you can take right now to help avoid regret in the last chapter of your life:

We’re all in this business of life together.

Let’s help each other make the journey shine like the ripples on our lake.

To Your Financial Freedom,

Roush Investment Group

O: 559.579.1490 F: (559) 490-2015 C: (559) 285-3318

What do we mean by the Holy Grail? And whose values? Yours or ours?

Regarded as a sacred object, the Holy Grail refers to the cup used by Jesus at the Last Supper; it is believed to possess miraculous powers to “provide happiness, eternal youth or sustenance in infinite abundance.” Whether real and lost to history or only a legend in literature, the quest for the Holy Grail is an apt metaphor for today’s post.

At the very heart of the relationship between advisor and client we find the oft unspoken quest for core values. You want to know your advisor’s core values. He or she wants to know yours. Why?

One word: Trust.

When embarking on a financial life journey together, client and advisor must trust one another. The presence of trust is the only way to remove the fear of risk, so often prevalent in financial decisions.

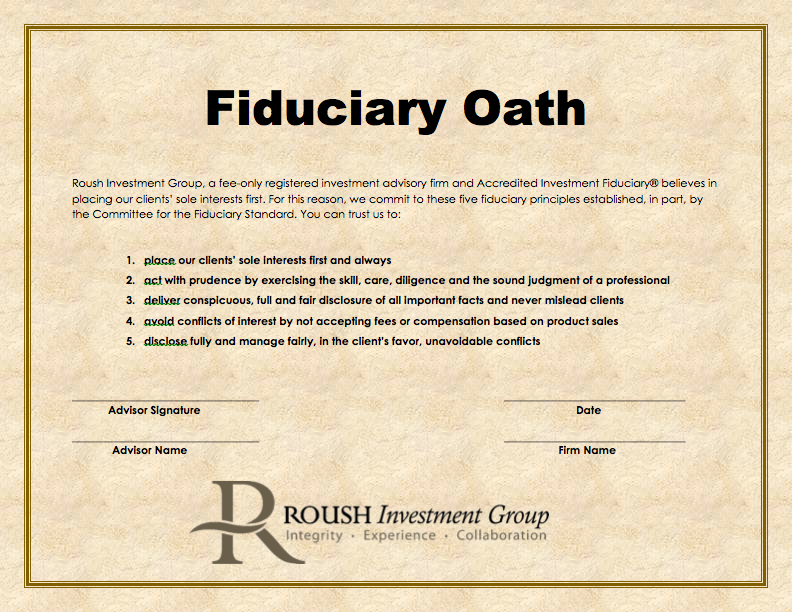

You meet with an advisor. He asks you to read his Fiduciary Oath. Is that sufficient? What more should you know?

He asks what you value in life and how you wish to express those values through your wealth. Is that sufficient? What more should he know?

In understanding our core values, we try to figure out the nature of our best selves. How to guide our behavior with a strong moral compass. How to treat people, clients, and each other.

While core values require an inward-focused search over time, outside events, pivotal people, and lifelong learning shape them, too. Let me ask a question.

Does a statement of values hung on an office wall or written into a Fiduciary Oath move you?

Many companies state core values in their public-facing documents: Communication. Respect. Integrity. Excellence. What do these words mean? They meant nothing to Enron in whose 2000 annual report they were printed.

Or are core values the embodiment of how we behave each day? How employees behave? What we do in a crisis? What we do in private and in public.

Core values, like the Holy Grail, are to be revered, protected and woven into life’s moments of truth.

For us, core values are critical to long-term growth and our business value. But they are not one dimensional. They matter because they build bonds of trust. With you and your family.

I worry about the financial services industry. Too many examples of rudderless, rogue advisors or ravenous banks have commanded headlines since 2008. Remember the '80s savings and loan crisis?

But we can and will stand apart. By following your core values. And our own.

As a client of Roush Investment Group, either on the wealth management or 401(k) plan side, you took a leap of faith that we would deliver on our promise. I’ll share a quote by Roy Disney: “It is not hard to make decisions when you know what your values are.”

You knew. And decided to join us. I hope not before we fully understood you as a person. Because deep understanding of our clients underscores our business purpose. Your unique beliefs, attitudes and behaviors matter to us.

Instead of asking you questions from a pro forma questionnaire, we try to ask the question behind the question.

These are but a few of hundreds of questions that go to the source of your core values. Your answers help us to hear you, see you and understand you.

Something we all want. To be heard, seen and understood. Don’t misunderstand. We are not psychologists. By any stretch. We deal with these questions because money can exercise power over the human mind. And money, especially wealth, can affect your core values.

Think for a moment about your core values. Here’s a short, random list some of the values our clients might share with us. Do you recognize any of your core values?

You’ll notice one value concept missing: Happiness.

Most clients value happiness and tell us wealth brings happiness, brings meaning.

The late Joseph Campbell, an extraordinary writer and lecturer on the human experience, saw life this way:

“People say that what we’re all seeking is a meaning for life. I don’t think that’s what we’re really seeking. I think that what we’re seeking is an experience of being alive.”

“People say that what we’re all seeking is a meaning for life. I don’t think that’s what we’re really seeking. I think that what we’re seeking is an experience of being alive.”

An experience of being fully alive.

With your core values to guide you on the journey.

It’s nothing less than perfect in a less than perfect world.

So how does the Roush team express its core values. Allow me:

1. In how we hire:

2. In how we behave:

3. In how we manage our firm:

4. In how we treat our clients:

Well, I’ve been a little philosophical in this post. Thank you for indulging me. My takeaway message?

Whomever you choose to advise you financially, anchor the relationship with shared core values.

To Your Financial Freedom,

Roush Investment Group

O: 559.579.1490 F: (559) 490-2015 C: (559) 285-3318

A clarion call went out to ERISA fiduciaries on June 9 when new fiduciary rule went into effect.

The Employee Retirement Income Security Act of 1974, or ERISA, protects the assets of millions of Americans so that funds placed in retirement plans during their working lives will be available when they retire. The IRS, Department of Labor, and ERISA regulate various compliance aspects of plans.

The fiduciary rule affects over half of the country’s working population. Participation in 401(k) plans continues to grow with more than 50 million workers actively participating in more than 500,000 different company plans. The Investment Company Institute reports Americans hold nearly five trillion dollars in assets in 401(k) plans at the end of 2016.

The compliance stakes are high.

A look back at 2013 alone shows the DOL collected from plan sponsors $1.69 billion in fines, voluntary fiduciary corrections, and informal complaint resolutions, which represents 33 percent increase over the previous year.

Many employers (plan sponsors) offering 401(k) plans do not realize they are personally liable for any compliance breach of their retirement plans. They may not even understand their fiduciary responsibilities because they assume service providers take care of this “administrative” detail.

That is a dangerous misconception.

Smaller plans with less than $50 million in assets face greater vulnerability because they may not understand the need for or role of designated fiduciaries. Unlike larger plans, smaller plans may not have in place elaborate compliance safety nets which protect larger plans. However, “ignorance of the law excuses no one” as the legal principle warns.

Arguably, there are half a dozen or more common compliance issues over which employers stumble:

Now, with the new fiduciary rule, employers not only have to worry about getting stuck in the weeds above, but they must also watch over the entire landscape.

In our last post, we discussed the new fiduciary rule and its requirement for advisors to act in the “best interest of clients.” This lifts the bar on the lower standard suitability followed by broker-dealers with the “potential for conflicted advice offerings” because they receive commissions on certain investment products.

“Plan sponsors, in their capacity as fiduciaries, should know whether or not their advisors are fiduciaries and whether they have any conflicts of interest,” says Fred Reish, known as the industry’s go-to ERISA expert.

“If I were on a plan committee, I would ask the adviser for a written answer to those two questions,” he urges.

Remember, many broker plan providers still operate under the suitability standard, which does not protect you from plan liability. You must step up.

Is anyone reviewing plan communications to ensure compliance with the fiduciary rule? Are your plan providers recommending specific IRAs or investments to plan participants in their rollover actions? Both potential landmines.

First, it is important plan sponsors review all relationships with investment advisors for their fiduciary status. If unclear, your litmus test is to secure a fiduciary pledge of assurance that they accept full investment responsibility for the plan.

Even so, as plan sponsor, you are still required to monitor their actions to ensure everything that could be done is being done in the best interest of the plan and your participants.

And, until January 1, 2018, you are in a bit of a twilight zone. That’s because one accountability part of the new fiduciary rule, called the Best Interest Contract Exemption (BICE), won’t be enforced until then. BICE permits employers to continue working with brokers who collect commissions if the broker agrees to act in a fiduciary capacity and disclose all forms of compensation.

Until then, the playing field remains gray as legal interpretation of key wording continues. Apparently, the new DOL fiduciary rule covers 1,000 pages.

Your best path is to undergo a fiduciary assessment now to know where you stand, what plan areas may be vulnerable, then act to avert possible hefty fines or burdensome litigation.

No doubt Fidelity, American Century, Franklin Templeton, Allianz, New York Life, and Cetera, to name a few in the financial sector alone, wish that had occurred before class-action suits made their way to the courts over their roles as plan sponsors.

As a registered investment advisor and 3(21) fiduciary, Roush Investment Group invites you to consider a full fiduciary assessment of your 401(k) plan to ensure it is compliant and penalty-free. Some of the key areas we analyze during this process include:

Armed with this information and corrective recommendations, you will be able to self-correct and bring your plan up to date with new DOL and IRS requirements.

You cannot put a price on peace of mind.

To Your Financial Freedom,

Roush Investment Group

O: 559.579.1490 F: (559) 490-2015 C: (559) 285-3318

On June 9, a quiet storm blew over the financial services industry.

Compliance with the long-awaited Department of Labor (DOL) fiduciary rule became a reality.

Now firms must comply with the fiduciary definition along with provisions on conflicts of interest and impartial conduct. Written disclosures requirements kick in Jan. 1, 2018.

What does this watershed moment mean to the industry?

Some observers expect the DOL to try to “overturn or modify the current rule.” Others predict that in “three to five years all advisors will be fiduciaries for both retirement and nonretirement accounts.”

Under pressure from both the rule and clients, many brokers, broker-dealer firms and wirehouses will scramble to shift from the “suitability standard” to the higher fiduciary standard of care, requiring advisors act in clients’ best interest.

This excerpt from a recent Forbes Magazine article explains the difference with a familiar car purchase analogy:

“Under the suitability standard, the dealer could say, “A Ford Explorer would meet all of your needs and we have some of those right over here.” The dealer makes the sale and gets the commission. You have a car that is suitable for your needs, but it isn’t necessarily what’s best for you. Since you don’t have a great deal of knowledge about the auto market, you are in the dark.

Under the fiduciary standard, the dealer would be obligated to say, “It sounds like you are describing a Toyota Highlander. We don’t sell those. In order to get exactly what you described, you would have to go down the street to Toyota and ask for a Highlander. I can sell you a similar model called a Ford Explorer, it’s more expensive and it isn’t exactly what you described.” In this scenario, you have more information about your options and the conflicts driving the dealer.

The Ford dealer has a clear conflict of interest in this situation. He can only sell Fords and will lose the opportunity to earn a commission if the client buys a Toyota Highlander. Under the suitability standard, the client ends up with a product (Ford Explorer) that isn’t the best fit given their situation and it costs more than the better-fitting product (Toyota Highlander). Worst of all, the client probably has no idea that they weren’t given advice that put their own interests first.”

And so it is, the difference between brokers (registered representatives) and RIAs (registered investment advisors) as explained in our last blog on why you must know the difference between RIAs and brokers.

And so it is, the difference between brokers (registered representatives) and RIAs (registered investment advisors) as explained in our last blog on why you must know the difference between RIAs and brokers.

Roush Investment Group opened its doors in 2010 as a 3(21) fiduciary; we’ve practiced in the sole interest of our clients from day one. As far as we’re concerned, the rest of the industry has arrived unfashionably late to the party.

The shift to a fiduciary standard of care is not for the faint of heart. A 2016 study by A.T. Kearney forecasts the industry will sacrifice $20 billion in lost revenue through 2020, as more informed clients want to do business with fiduciaries. In fact, it is expected up to $2 trillion in assets will shift among different firms.

But here’s the rub. The rule is not a mandate. “By and large, absent a government mandate, you’ll find firms holding strong and trying not to deliver advice under a fiduciary standard,” predicts Brian Hamburger, president and CEO of MarketCounsel, a business and regulatory consulting firm for investment advisors.

But here’s the rub. The rule is not a mandate. “By and large, absent a government mandate, you’ll find firms holding strong and trying not to deliver advice under a fiduciary standard,” predicts Brian Hamburger, president and CEO of MarketCounsel, a business and regulatory consulting firm for investment advisors.

In an interview with Barron’s, Hamburger shared his belief that most firms will stick to the status quo unless forced to change because the old ways are more profitable.

And the only force that can force a change is the Securities and Exchange Commission (SEC), which holds power to create a uniform regulatory standard governing the behavior of all brokers and investment advisors. One can speculate such a standard is the only way “we’re going to see the best investor protection possible,” says Charles Goldman, CEO of AssetMark.

Objectively, the new fiduciary rule may not automatically guarantee the full protection clients seek. First, the DOL “continues to look at the rule’s wording and aren’t promising they won’t change it. In fact, this is one of the reasons they used to justify any enforcement until the start of next year,” explains Chris Carosa on BenefitsPro.com. Second, pundits agree the rule has loopholes, which could lead to abuses.

In my opinion, you still need to rely on your instincts about who is and who is not a “trusted advisor.” He or she may operate as a fiduciary. But what if they fall short in integrity, expertise, critical thinking, authenticity, insight or caring? No rule can compensate for these deficiencies.

Rest easy. You, your family, your business, and accounts are carefully wrapped in the best protection possible. We have always operated in your sole interest under the fiduciary standard of care.

Remember, I once came from the other side. When we launched our firm, I knew what to do to build a wall of protection around my clients because I’ve witnessed firsthand the consequences of working with people driven only by the profit motive. Pushing proprietary products. Hidden fees and commissions. Risky investments. These are nowhere in our DNA.

For business owners (plan sponsors) offering 401(k) plans through us, you, too, are fiduciaries.

In our next post, we’ll talk about what you need to do to ensure you remain in compliance.

Better yet, this may be the ideal time to consider a compliance audit on your retirement plan.

Don’t risk hefty fines and litigation. We’re here to protect you.

To Your Financial Freedom,

Roush Investment Group

O: 559.579.1490 F: (559) 490-2015 C: (559) 285-3318

An ominous gray cloud continues to form overhead.

Before you get caught in a storm burst, we want you to know how to protect yourself.

In the next few paragraphs, I’ll define some valuable terms:

Allow me first to explain the various (confusing) business models or channels by which our industry operates. Sophisticated investors, please excuse the 101 lesson. For others, knowledge is power.

Our industry overcomplicates itself with definitions. Many models exist: Retail banks; Wirehouses (full-service brokerages) like Bank of America’s Merrill Lynch, Morgan Stanley Smith Barney, UBS and Wells Fargo; Regional firms like Raymond James or Ameriprise Financial. Boutiques like Credit Suisse; Discount brokerages like Scott Trade; Multi-family offices for intergenerational wealth.

I want to focus on two key channels. First, Broker-Dealers (B-Ds). BD “advisors” are independent contractors and do business under their firm name or a larger BD, like LPL for back-office support.

Regulated by FINRA, the Financial Industry Regulatory Authority, B-Ds comprise members from the industry who, in effect, self-regulate. Banks own many broker-dealers, and they follow the “suitability” standard─investments made on behalf of a client must be suitable for the client at the time purchased. Further, they are fee-based, not fee-only, which means they can charge clients a fee to develop a financial plan, then charge more fees (or commissions) to implement the plan.

Registered Investment Advisors (RIAs). The RIA model came about after the Great Depression ended in 1939, presumably as a protective reaction to massive investor losses. RIAs hold a “fiduciary duty” to clients, which means they are legally obligated to always act in the “best interest” of clients, a major differentiator from B-Ds.

Under a fiduciary standard of care, your RIA must ensure the appropriateness of any risky investment under all circumstances. The Securities and Exchange Commission (SEC) or state regulatory bodies regulate RIAs under the 1940 Investment Advisors Act.

True RIAs are fee-only advisors, another major differentiator, and do not accept any fees or compensation based on product sales, which means no inherent conflicts of interest. Clients agree in advance to a fee tied to the value of the assets for management of the account, the only fee charged. No trailing commissions on mutual funds. No hidden fees on anything. Full stop.

While I admit to bias, RIAs provide more comprehensive advice, in part, because they are duty bound to clients to show transparency, impartiality, and full-disclosure of fees. Always know the compensation mechanism of your advisor.

Roush Investment Group operates as a RIA, working in your sole and best interest. RIAs give up their Series 7 securities licenses. If we fail our fiduciary duty, we can go to prison. No other business model in the industry─except the RIA─follows the higher fiduciary standard of care, signs an oath to adhere it, and faces criminal charges if it fails to meet the standard.

Another channel has emerged in recent years: Hybrid Advisor. And here is where it gets complicated for clients. Dually registered with FINRA and the SEC, hybrids have the option to take any business, whether fee-based or commissioned, even with the same client. Yes, you have a choice on how to be charged. And, yes, you can access many products or services from a variety of firms.

But you may never know when the hybrid decides to push a “suitable” product to you for higher commission or decides instead to offer you fee-based advice because they:

Broker-dealers may state they support the fee side of the business; a hollow declaration because they stand to earn substantially more money if their reps sell commission products. At your expense.

Given a choice between making more money and doing the right thing? After all, there’s a reason why greed is one of the seven deadly sins.

What’s more, broker-dealers owned by banks do not want the liability exposure of a fiduciary standard of care. Suitability works fine for them. However, clients realize no benefit. In fact, the entire hybrid structure does not benefit the client, only the hybrid “advisor.”

Please understand, an ocean of difference exists between the prudent recommendations of a RIA and the suitable recommendations of a hybrid, fee-based advisor.

The impetus behind the hybrid channel is the broker-dealer. It uses the channel as a flexibility magnet to attract and hold those advisors who do not want to tether to only a broker-dealer or RIA.

I’m not saying they are “bad actors” in an industry already fraught with trust issues; I am saying caveat emptor, buyer beware.

You can get out from under the gray cloud of uncertainty. You can adopt certain protective gear. No matter from whom you seek financial advice, ask the following questions and clear the air. If the person at the other end of the question hesitates at all, or succeeds in hedging an answer altogether, he or she likely has a conflict of interest and is not operating in your best interest.

1. Are you familiar with the Fiduciary Oath from the Committee for the Fiduciary Standard?

If, yes, continue with next question. If no, walk away.

2. Describe for me your Fiduciary Oath and would you sign it for me?

If, yes, continue with next question. If no, walk away.

3. Are you affiliated with a broker-dealer? Or a bank?

If, yes, continue with next question. If no, continue to probe.

4. Can you tell me what to expect from products or services?

Listen very carefully and take notes.

5. Are there any disclosed or non-disclosed benefits or commissions which accrue to you?

Depending on the answer, reconsider working with the advisor to protect your money from fee erosion. Banks and broker-dealers hide fees.

We do not believe your interests should be subordinated to the financial interests of the industry.

We do believe anyone calling himself or herself a financial advisor or consultant should be held the fiduciary standard of conduct.

And, we believe you deserve the tools necessary to distinguish between higher-quality advisors and lower-quality advisors.

This email address is being protected from spambots. You need JavaScript enabled to view it. with a simple “I want the Fiduciary Oath,” and we will send it to you shortly to help you with questioning advisors.

In our next post, I’ll discuss the new Department of Labor Fiduciary Rule which went into partial effect June 9 and its implications for retirement plans and the investment advisory business.

© 2026 Roush Investment Group. All Rights Reserved.

Website Developed by WebCity Press.